Commodities Update May 2024

Commodities rallied through April as iron ore lifted on speculation of further Chinese housing support while base metals continued a bounce from their recent price correction. There was a partial offset from a decline in crude oil prices as geopolitical tensions swing between escalation and de-escalation while the supply outlook is more positive combined with a less constructive demand outlook.

The following is based on text from the Westpac May 2024 Market Outlook (PDF 420KB)

For more details of our longer-term forecasts see Westpac May 2024 Commodity Forecasts

Overall, April was a positive month for commodities with the Westpac Export Price Index rallying 7.1% since the last report. Iron ore is leading the charge with a solid 17.3% gain in the month supported by thermal coal (11.5%) and met coal (2%) that were only partially offset by a –6.5% fall in crude oil prices. There was also a solid rally in base metals with our Metals Index up 7.6% in the month with nickel (+14.6%) and zinc (+14.6%) leading the charge, all important copper not too far behind (+8.2%) while aluminium put in a solid performance (+5.7%). This month we have left our forecasts broadly unchanged with only minor marking-to-market for some near-term forecasts.

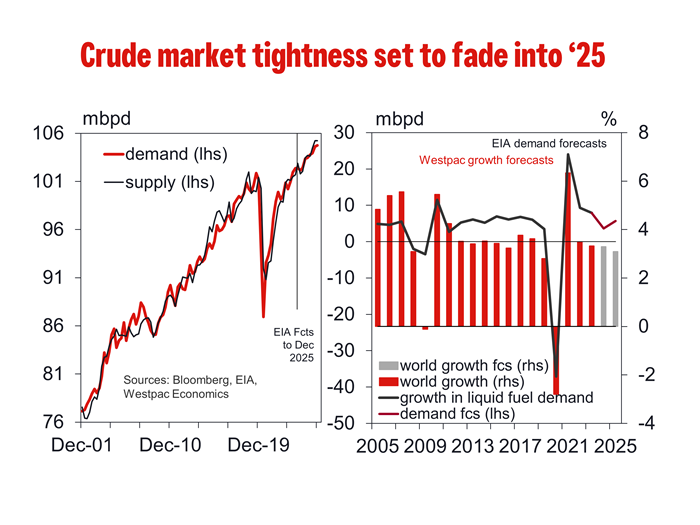

Crude oil: demand outlook has been revised down while the geopolitical outlook remains uncertain.

We continue to hold the view that near term geopolitical issues have been supportive of crude oil prices. As supply continues to outpace demand (the IEA has forecast a soft global demand growth estimate for 2024 of 1.2 million bpd), we expect crude prices to soften back towards US$78/bbl by early 2025.

For the near-term, we see crude capped around US$85/bbl as geopolitical developments remain at the fore. Israel’s war cabinet voted to “continue operations in Rafah to exert military pressure on Hamas in order to promote the release of our hostages and the other goals of war”. Scenes of tanks rolling through the Rafah crossing would certainly add to risks of a wider conflagration. Against this, there have been signs that we are moving incrementally towards an agreement between Israel and Hamas. Around demand weakness, Wood Mackenzie is forecasting this year to see the slowest growth for gasoline demand since 2020 (+340k bpd vs. +700k bpd in 2023), as China nears peak transport fuel demand while the US has passed peak demand.

OilChem (a provider of Chinese energy and chemical information and prices) reported that China was issuing a second quota for fuel exports as the nation faces a ballooning surplus amid faster adoption of clean energy vehicles. In addition, OilChem has also reported authorities had given permission to export 14 million tonnes of diesel, gasoline and jet fuel following the first batch of 19 million tonnes. That compares with 9 million tonnes for a second batch last year and 18.99 million tonnes for a first batch, representing a year-to-date rise of 18%. ADNOC (the Abu Dhabi energy group) confirmed it has ‘officially’ raised its production capacity from 4.65m bpd to 4.85m bpd (the by-product of a five year $150bn spending plan announced in 2022). This is in conflict with the current OPEC production quotas so there will be much in interest in the June 1 OPEC meeting in Vienna to see how this tension is reconciled.

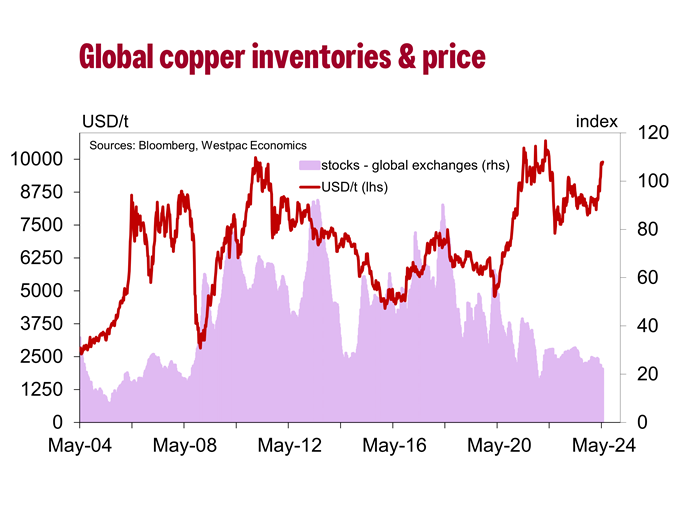

Base metals – appear stretched to fundamentals.

For base metals, we are still not convinced of the strength in the current rally, particularly for copper as it eye’s a US$9,500-10,000/t range. Firstly, our ‘rough’ estimates suggest the combined raw copper production of the top three producers (Chile, Peru and the Democratic Republic of Congo) is up 2.5%yr over January-February with a 5% surge in February alone. This is a far more positive start to the year than had been expected. In terms of refined copper production, Chinese production was up 12.4% in the year to March and 35% higher in the first quarter compared to the Q1 average over the last five years. The Yangshan physical premium paid on imported refined copper into China briefly hit zero last week for the first time on daily data back to 2017, pointing to “extremely weak demand for imported cargoes”. Further, Bloomberg reported that China’s copper exports are set to hit the highest in two years as “beleaguered smelters ship out metals to benefit from a powerful rally in global prices”.

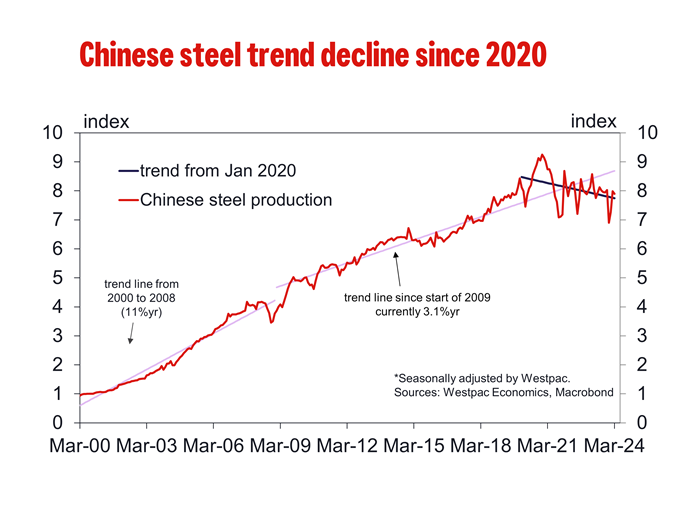

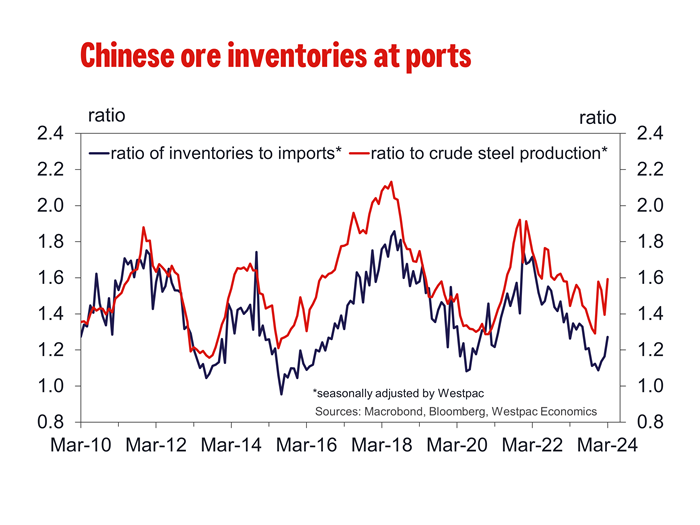

Iron ore – current strength likely to be short lived.

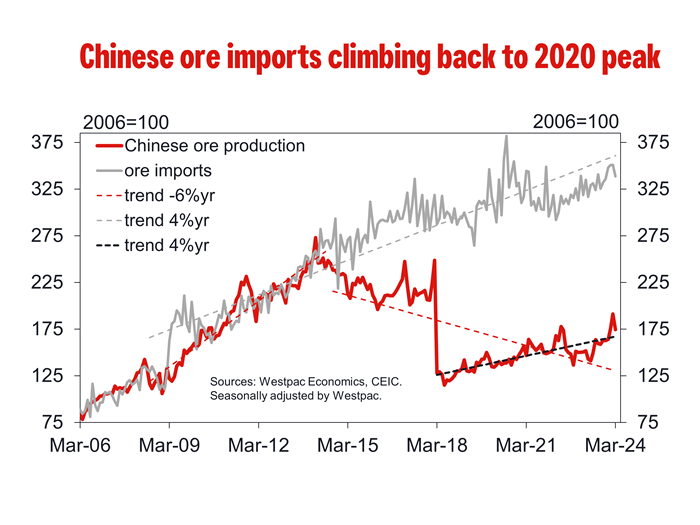

Turning to iron ore, we continue to expect any near-term strength to be capped around US$120/t though we see few reasons to expect a sudden reversal. Inventories of iron ore at Chinese ports are currently at a two-year high and more than one standard deviation above seasonal averages. In March, Chinese steel exports surged 25% year on year to 9.88 million tonnes, the strongest seen since July 2016. The US, Brazil, Chile and Mexico have all announced tariffs and/or quotas on Chinese steel, putting Chinese ‘dumping of surplus steel’ firmly on the political agenda. However, it has been reported that at a recent Politburo meeting, it was suggested that officials are researching ways to deal with stock of unsold properties in China, further raising optimism of a turnaround in the construction industry and triggering a huge rise in mainland property stocks.

While all the above will be supportive of near-term pricing, supply is improving while demand is softening. To March, imports of iron ore are up 5.4% year-to-date while Chinese ore production is up 20% year-to-date. We also note the very soft start to China’s steel production with pig iron production down –2.4% year-to-date in March while crude steel production was down 3.5%. As such, we hold to the view that iron ore prices will soften in the second half of 2024 to US$85/t by the end of the year.

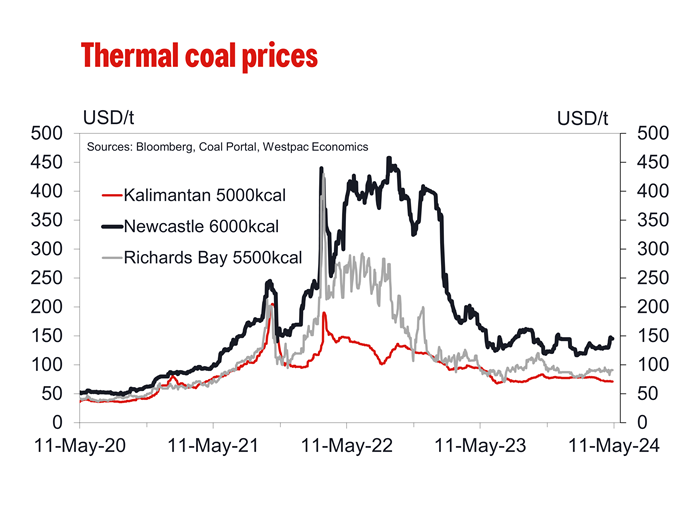

Thermal coal – prices have returned to pre-war levels.

Thermal coal prices reached unprecedented levels in 2022 after Russia invaded Ukraine, due to materially higher gas prices, trade flow disruption and supply disruption in Australia, Colombia, South Africa and Russia. Despite the record high prices, coal capex remains depressed with excess cash flows being used to deleverage or being returned to shareholders. Gas prices have eased, trade flows have largely adjusted, and prices are back to pre-war levels.

Stay informed with Westpac IQ

Get the latest reports straight to your inbox.

Related articles

Commodities Update February 2026

Browse topics

Disclaimer

©2026 Westpac Banking Corporation ABN 33 007 457 141 (including where acting under any of its Westpac, St George, Bank of Melbourne or BankSA brands, collectively, “Westpac”). References to the “Westpac Group” are to Westpac and its subsidiaries and includes the directors, employees and representatives of Westpac and its subsidiaries.

Things you should know

We respect your privacy: You can view the New Zealand Privacy Policy here, or the Australian Group Privacy Statement here. Each time someone visits our site, data is captured so that we can accurately evaluate the quality of our content and make improvements for you. We may at times use technology to capture data about you to help us to better understand you and your needs, including potentially for the purposes of assessing your individual reading habits and interests to allow us to provide suggestions regarding other reading material which may be suitable for you.

This information, unless specifically indicated otherwise, is under copyright of the Westpac Group. None of the material, nor its contents, nor any copy of it, may be altered in any way, transmitted to, copied of distributed to any other party without the prior written permission of the Westpac Group.

Disclaimer

This information has been prepared by Westpac and is intended for information purposes only. It is not intended to reflect any recommendation or financial advice and investment decisions should not be based on it. This information does not constitute an offer, a solicitation of an offer, or an inducement to subscribe for, purchase or sell any financial instrument or to enter into a legally binding contract. To the extent that this information contains any general advice, it has been prepared without taking into account your objectives, financial situation or needs and before acting on it you should consider the appropriateness of the advice. Certain types of transactions, including those involving futures, options and high yield securities give rise to substantial risk and are not suitable for all investors. We recommend that you seek your own independent legal or financial advice before proceeding with any investment decision.

This information may contain material provided by third parties. While such material is published with the necessary permission none of Westpac or its related entities accepts any responsibility for the accuracy or completeness of any such material. Although we have made every effort to ensure this information is free from error, none of Westpac or its related entities warrants the accuracy, adequacy or completeness of this information, or otherwise endorses it in any way. Except where contrary to law, Westpac Group intend by this notice to exclude liability for this information. This information is subject to change without notice and none of Westpac or its related entities is under any obligation to update this information or correct any inaccuracy which may become apparent at a later date. This information may contain or incorporate by reference forward-looking statements. The words “believe”, “anticipate”, “expect”, “intend”, “plan”, “predict”, “continue”, “assume”, “positioned”, “may”, “will”, “should”, “shall”, “risk” and other similar expressions that are predictions of or indicate future events and future trends identify forward-looking statements. These forward-looking statements include all matters that are not historical facts. Past performance is not a reliable indicator of future performance, nor are forecasts of future performance. Whilst every effort has been taken to ensure that the assumptions on which any forecasts are based are reasonable, the forecasts may be affected by incorrect assumptions or by known or unknown risks and uncertainties. The ultimate outcomes may differ substantially from any forecasts.

Conflicts of Interest: In the normal course of offering banking products and services to its clients, the Westpac Group may act in several capacities (including issuer, market maker, underwriter, distributor, swap counterparty and calculation agent) simultaneously with respect to a financial instrument, giving rise to potential conflicts of interest which may impact the performance of a financial instrument. The Westpac Group may at any time transact or hold a position (including hedging and trading positions) for its own account or the account of a client in any financial instrument which may impact the performance of that financial instrument.

Author(s) disclaimer and declaration: The author(s) confirms that (a) no part of his/her compensation was, is, or will be, directly or indirectly, related to any views or (if applicable) recommendations expressed in this material; (b) this material accurately reflects his/her personal views about the financial products, companies or issuers (if applicable) and is based on sources reasonably believed to be reliable and accurate; (c) to the best of the author’s knowledge, they are not in receipt of inside information and this material does not contain inside information; and (d) no other part of the Westpac Group has made any attempt to influence this material.

Further important information regarding sustainability-related content: This material may contain statements relating to environmental, social and governance (ESG) topics. These are subject to known and unknown risks, and there are significant uncertainties, limitations, risks and assumptions in the metrics, modelling, data, scenarios, reporting and analysis on which the statements rely. In particular, these areas are rapidly evolving and maturing, and there are variations in approaches and common standards and practice, as well as uncertainty around future related policy and legislation. Some material may include information derived from publicly available sources that have not been independently verified. No representation or warranty is made as to the accuracy, completeness or reliability of the information. There is a risk that the analysis, estimates, judgements, assumptions, views, models, scenarios or projections used may turn out to be incorrect. These risks may cause actual outcomes to differ materially from those expressed or implied. The ESG-related statements in this material do not constitute advice, nor are they guarantees or predictions of future performance, and Westpac gives no representation, warranty or assurance (including as to the quality, accuracy or completeness of the statements). You should seek your own independent advice.

Additional country disclosures:

Australia: Westpac holds an Australian Financial Services Licence (No. 233714). You can access Westpac’s Financial Services Guide here or request a copy from your Westpac point of contact. To the extent that this information contains any general advice, it has been prepared without taking into account your objectives, financial situation or needs and before acting on it you should consider the appropriateness of the advice.

New Zealand: In New Zealand, Westpac Institutional Bank refers to the brand under which products and services are provided by either Westpac (NZ division) or Westpac New Zealand Limited (company number 1763882), the New Zealand incorporated subsidiary of Westpac ("WNZL"). Any product or service made available by WNZL does not represent an offer from Westpac or any of its subsidiaries (other than WNZL). Neither Westpac nor its other subsidiaries guarantee or otherwise support the performance of WNZL in respect of any such product. WNZL is not an authorised deposit-taking institution for the purposes of Australian prudential standards. The current disclosure statements for the New Zealand branch of Westpac and WNZL can be obtained at the internet address www.westpac.co.nz.

Singapore: This material has been prepared and issued for distribution in Singapore to institutional investors, accredited investors and expert investors (as defined in the applicable Singapore laws and regulations) only. Recipients of this material in Singapore should contact Westpac Singapore Branch in respect of any matters arising from, or in connection with, this material. Westpac Singapore Branch holds a wholesale banking licence and is subject to supervision by the Monetary Authority of Singapore.

Fiji: Unless otherwise specified, the products and services for Westpac Fiji are available from www.westpac.com.fj © Westpac Banking Corporation ABN 33 007 457 141. This information does not take your personal circumstances into account and before acting on it you should consider the appropriateness of the information for your financial situation. Westpac Banking Corporation ABN 33 007 457 141 is incorporated in NSW Australia and registered as a branch in Fiji. The liability of its members is limited.

Papua New Guinea: Unless otherwise specified, the products and services for Westpac PNG are available from www.westpac.com.pg © Westpac Banking Corporation ABN 33 007 457 141. This information does not take your personal circumstances into account and before acting on it you should consider the appropriateness of the information for your financial situation. Westpac Banking Corporation ABN 33 007 457 141 is incorporated in NSW Australia. Westpac is represented in Papua New Guinea by Westpac Bank - PNG - Limited. The liability of its members is limited.

U.S.: Westpac operates in the United States of America as a federally licensed branch, regulated by the Office of the Comptroller of the Currency. Westpac is also registered with the US Commodity Futures Trading Commission (“CFTC”) as a Swap Dealer, but is neither registered as, or affiliated with, a Futures Commission Merchant registered with the US CFTC. The services and products referenced above are not insured by the Federal Deposit Insurance Corporation (“FDIC”). Westpac Capital Markets, LLC (‘WCM’), a wholly-owned subsidiary of Westpac, is a broker-dealer registered under the U.S. Securities Exchange Act of 1934 (‘the Exchange Act’) and member of the Financial Industry Regulatory Authority (‘FINRA’). In accordance with APRA's Prudential Standard 222 'Association with Related Entities', Westpac does not stand behind WCM other than as provided for in certain legal agreements between Westpac and WCM and obligations of WCM do not represent liabilities of Westpac.

This communication is provided for distribution to U.S. institutional investors in reliance on the exemption from registration provided by Rule 15a-6 under the Exchange Act and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors in the United States. WCM is the U.S. distributor of this communication and accepts responsibility for the contents of this communication. Transactions by U.S. customers of any securities referenced herein should be effected through WCM. All disclaimers set out with respect to Westpac apply equally to WCM. If you would like to speak to someone regarding any security mentioned herein, please contact WCM on +1 212 389 1269. Investing in any non-U.S. securities or related financial instruments mentioned in this communication may present certain risks. The securities of non-U.S. issuers may not be registered with, or be subject to the regulations of, the SEC in the United States. Information on such non-U.S. securities or related financial instruments may be limited. Non-U.S. companies may not be subject to audit and reporting standards and regulatory requirements comparable to those in effect in the United States. The value of any investment or income from any securities or related derivative instruments denominated in a currency other than U.S. dollars is subject to exchange rate fluctuations that may have a positive or adverse effect on the value of or income from such securities or related derivative instruments.

The author of this communication is employed by Westpac and is not registered or qualified as a research analyst, representative, or associated person of WCM or any other U.S. broker-dealer under the rules of FINRA, any other U.S. self-regulatory organisation, or the laws, rules or regulations of any State. Unless otherwise specifically stated, the views expressed herein are solely those of the author and may differ from the information, views or analysis expressed by Westpac and/or its affiliates.

UK: The London branch of Westpac is authorised in the United Kingdom by the Prudential Regulation Authority (PRA) and is subject to regulation by the Financial Conduct Authority (FCA) and limited regulation by the PRA (Financial Services Register number: 124586). The London branch of Westpac is registered at Companies House as a branch established in the United Kingdom (Branch No. BR000106). Details about the extent of the regulation of Westpac’s London branch by the PRA are available from us on request.

This communication is not being made to or distributed to, and must not be passed on to, the general public in the United Kingdom. Rather, this communication is being made only to and is directed at (a) those persons falling within the definition of Investment Professionals (set out in Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”)); (b) those persons falling within the definition of high net worth companies, unincorporated associations etc. (set out in Article 49(2)of the Order; (c) other persons to whom it may lawfully be communicated in accordance with the Order or (d) any persons to whom it may otherwise lawfully be made (all such persons together being referred to as “relevant persons”). Any person who is not a relevant person should not act or rely on this communication or any of its contents. In the same way, the information contained in this communication is intended for “eligible counterparties” and “professional clients” as defined by the rules of the Financial Conduct Authority and is not intended for “retail clients”. Westpac expressly prohibits you from passing on the information in this communication to any third party.

European Economic Area (“EEA”): This material may be distributed to you by either: (i) Westpac directly, or (ii) Westpac Europe GmbH (“WEG”) under a sub-licensing arrangement. WEG has not edited or otherwise modified the content of this material. WEG is authorised in Germany by the Federal Financial Supervision Authority (‘BaFin’) and subject to its regulation. WEG’s supervisory authorities are BaFin and the German Federal Bank (‘Deutsche Bundesbank’). WEG is registered with the commercial register (‘Handelsregister’) of the local court of Frankfurt am Main under registration number HRB 118483. In accordance with APRA’s Prudential Standard 222 ‘Association with Related Entities’, Westpac does not stand behind WEG other than as provided for in certain legal agreements (a risk transfer, sub-participation and collateral agreement) between Westpac and WEG and obligations of WEG do not represent liabilities of Westpac. Any product or service made available by WEG does not represent an offer from Westpac or any of its subsidiaries (other than WEG). All disclaimers set out with respect to Westpac apply equally to WEG.

This communication is not intended for distribution to, or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation.

This communication contains general commentary, research, and market colour. The communication does not constitute investment advice. The material may contain an ‘investment recommendation’ and/or ‘information recommending or suggesting an investment’, both as defined in Regulation (EU) No 596/2014 (including as applicable in the United Kingdom) (“MAR”). In accordance with the relevant provisions of MAR, reasonable care has been taken to ensure that the material has been objectively presented and that interests or conflicts of interest of the sender concerning the financial instruments to which that information relates have been disclosed.

Investment recommendations must be read alongside the specific disclosure which accompanies them and the general disclosure which can be found here. Such disclosure fulfils certain additional information requirements of MAR and associated delegated legislation and by accepting this communication you acknowledge that you are aware of the existence of such additional disclosure and its contents.

To the extent this communication comprises an investment recommendation it is classified as non-independent research. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and therefore constitutes a marketing communication. Further, this communication is not subject to any prohibition on dealing ahead of the dissemination of investment research.