Markets Daily

Further gains in the US dollar and bond yields were helped by hawkish comments from Fed Chair Powell and solid US industrial production data.

Currencies/Macro

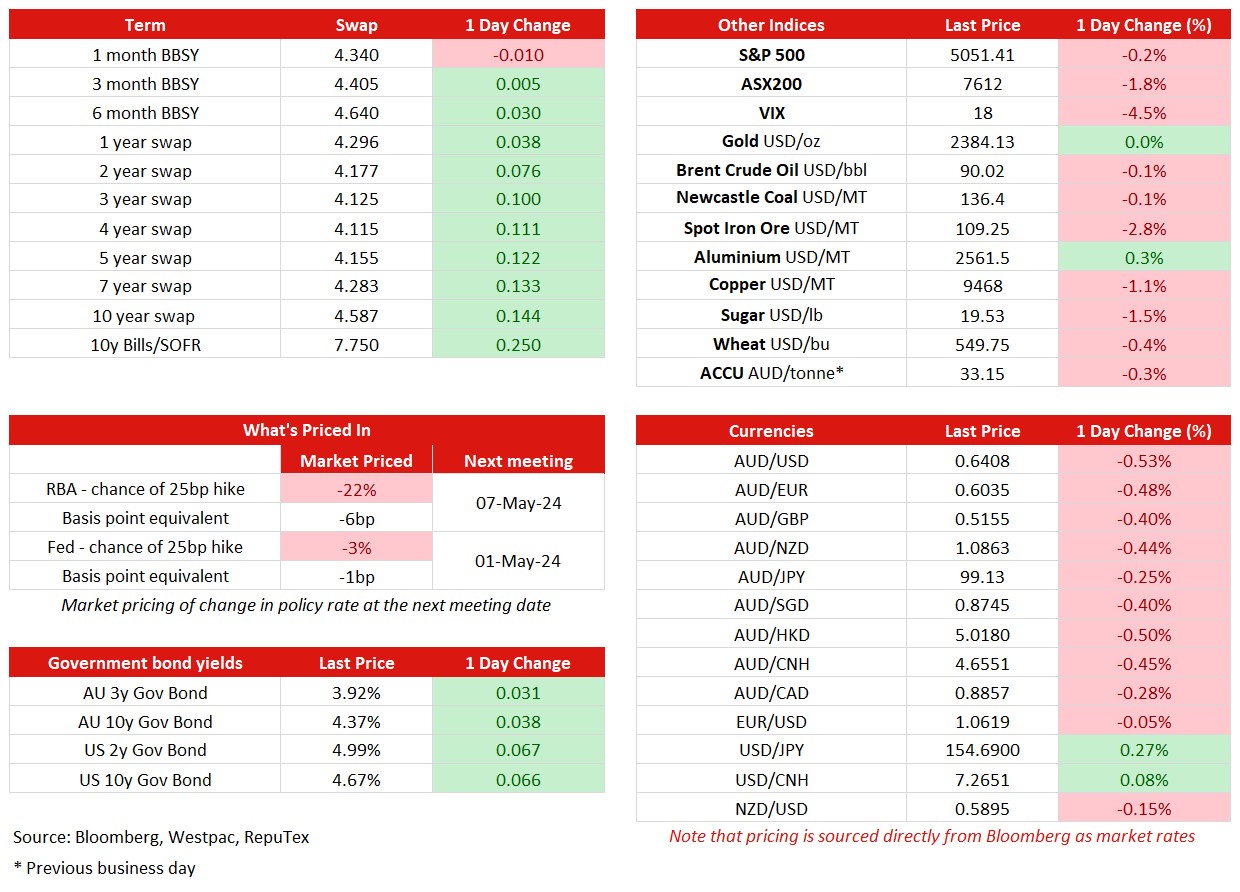

The US dollar index is up 0.1% on the day, and at a fresh six-month high, supported by higher US bond rates after Fed Chair Powell said more patience is required to regain confidence that inflation is moving lower. EUR ranged between 1.0601 and 1.0654. USD/JPY rose from 154.30 to 154.79 – a fresh 34-year high.

Underperformer AUD fell from 0.6425 to 0.6389 - a fresh five-month low. Stronger China Q1 GDP provided no support for AUD yesterday, with markets instead fixated on the PBOC acceding to market pressures and setting a higher reference for USD/CNY, weighing on regional currencies. NZD fell from 0.5895 to 0.5868 – a fresh five-month low. AUD/NZD fell from 1.0910 to 1.0882.

Fed Chair Powell indicated they could wait longer than previously expected to cut interest rates following a series of surprisingly high inflation readings: “The recent data have clearly not given us greater confidence and instead indicate that is likely to take longer than expected to achieve that confidence. Given the strength of the labour market and progress on inflation so far, it is appropriate to allow restrictive policy further time to work and let the data and the evolving outlook guide us”.

US industrial production in March rose 0.4%m/m (as expected, prior revised to +0.4%m/m from +0.1%m/m), with a notable rise in manufacturing of 0.5%mm (est. +0.2%m/m. prior revised higher to +1.1%m/m from +0.8%m/m. Capacity utilisation was at 78.4% (est. 75.5%, prior revised to 78.2% from 78.3%). Housing starts fell 14.7% (est. -2.4%) and building permits fell 4.3% (est. -0.9%).

Canada’s CPI in March rose 0.6%m/m and 2.9%y/y (est. 0.7% and 2.9%, prior 2.8%y/y), with trimmed core at 3.1%y/y (est. 3.2%, prior 3.2%).

The ZEW investor surveys were stronger than expected. German expectations rose to +42.9 (est. +35.5, prior +31.7), current conditions to -79.2 (est. -76.0, prior -80.5). Eurozone expectations rose to +43.9 (prior +33.5), current conditions to -48.8 (prior -54.8).

UK unemployment in February was at 4.2% (est. 4.0%, prior 3.9%), but average weekly earnings were firm at 5.6%y/y (est. 5.5%, prior 5.6%).

The IMF upgraded its global growth forecasts, consistent with a global soft landing. 2024 was increased to 3.2% from 3.1%, and 2025 was increased to 3.2%. The US is the main contributor to the upgrades.

Interest rates

Powell’s comments and US data helped US treasury yields rise to highs since November. The US 2yr treasury yield rose from 4.92% to 4.97% via 5.01%, while the 10yr yield rose from 4.61% to 4.67% via 4.69%. Markets price the Fed funds rate, currently 5.375% (mid), to be unchanged at the next meeting on 2 May, with a 45% chance of a cut in July.

Australian government bond yields (futures) rose from 3.85% to 3.89%, while the 10yr yield rose from 4.32% to 4.37%. Markets currently price the RBA cash rate to be unchanged at the next meeting on 7 May, with a 60% chance of a cut by November.

New Zealand rates markets price the OCR, currently at 5.50%, to be unchanged at the next meeting on 22 May, with a 55% chance of a cut in August.

Despite geopolitical concerns, European primary markets were busy with six names issuing across the corporate and financials sector with covered bond issuance from Banca Monte dei Paschi and Equitable Bank. It was relatively quiet in the US with the only high grade issuance coming from Johnson Controls and Hana Bank. Itraxx Europe widened 2.7bps to 62.8bps with Zurich Insurance and Equinor were the best performing contracts and Lufthansa and Unibail- Rodamco- Westfield underperformed. CDX IG widened 0.3bps to 57.8bps; United Health and Johnson Controls had the best performing contracts while Ally Financial and Lincoln National were a drag on the index. Cash bonds widened 0.5ps to 124.2, the best performing sectors were industrials and utilities, while subordinated financials and communications.

Commodities

Crude markets marked time as traders waited for a response from Israel to the first ever wave of direct drone and missile strikes from Iran over the weekend. The May WTI contract is down 0.15% at $85.28 while the June Brent contract is down 0.18% at $89.94. Top Israeli military officials stated that “missiles into the territory of the State of Israel will be met with a response”. However, the “higher for longer” message from Fed Chair Powell and jump in the US$ capped recent moves. Bloomberg also noted that refiners in China and Korea were reducing run rates on lower margins and maintenance. API also reported a 4.09mn rise in crude inventory though gasoline again fell by 2.5mb. The May June European diesel spread flipped into contango. Excluding expiry days, that’s the first time that has happened in 11 months suggesting the impact of reduced Russian supplies is becoming more muted and that demand is slowing as economic activity wanes. On that point. France reported road diesel sales declined by 12% in March.

Metals were mixed with copper down just over 1% at $9,474 though aluminium held at fresh 14 month closing highs. Rio’s head of copper, Bold Baatar told the CRU World Copper Conference in Santiago that “the focus is on organic growth [and] supply growth”. Rio is looking to reach 1mtpa of copper production in 5yrs, up from 700kt with projects in Mongolia, Utah and a joint venture with Codelco in Chile all adding to global supply. Aluminium was more contained after the aggressive moves higher seen the previous session following the US sanctions on trading Russian aluminium, copper and nickel. The new rules prohibit delivery of new supplies from Russia into the LME on or after April 13 while the US is also banning the import of all three metals from Russia. The price for spot versus 3-month aluminium spread on the LME surged as traders reacted to the fact that the changes do not prevent Russia from selling its metals to buyers outside the US or UK.

Finally note that iron ore showed some signs of settling back from the recent aggressive run up from below $100 to above $110. The May SGX contract is down $1 from the same time yesterday at $110.85 while the 62% Mysteel index is down $3.1 at $109.25. While Q1 China GDP beat expectations, steel production in March came in at 88mt, down almost 8% from the previous month. Meanwhile Vale announced iron ore production came in above expectations at 70.8mt though Rio missed expectations shipping 78mt. BHP will report tomorrow.

Day ahead

Aus: March's Westpac–MI Leading Indexcould reflect a pull-back in commodity prices.

NZ: Q1 CPI will show domestic forces driving prices with headline and core rates still above the RBNZ's mid-point (Westpac f/c: 4.2%yr, market f/c: 4.0%yr). March's REINZ house sales are expected to lift following a surge in listings. Prices will likely be capped as a result.

Eurozone/UK: The UK's March CPI will show continued strength in services driving headline inflation (market f/c: 3.1%yr). The final estimate for Europe's March CPI will be released (market f/c: 2.4%yr).

US: The FOMC’s Beige Book provides an update on economic conditions across the regions. Mester will also speak today.

Related articles

Browse topics

Disclaimer

©2024 Westpac Banking Corporation ABN 33 007 457 141 (including where acting under any of its Westpac, St George, Bank of Melbourne or BankSA brands, collectively, “Westpac”). References to the “Westpac Group” are to Westpac and its subsidiaries and includes the directors, employees and representatives of Westpac and its subsidiaries.

Things you should know

We respect your privacy: You can view our privacy statement at Westpac.com.au. Each time someone visits our site, data is captured so that we can accurately evaluate the quality of our content and make improvements for you. We may at times use technology to capture data about you to help us to better understand you and your needs, including potentially for the purposes of assessing your individual reading habits and interests to allow us to provide suggestions regarding other reading material which may be suitable for you.

This information, unless specifically indicated otherwise, is under copyright of the Westpac Group. None of the material, nor its contents, nor any copy of it, may be altered in any way, transmitted to, copied of distributed to any other party without the prior written permission of the Westpac Group.

Disclaimer

This information has been prepared by the Westpac and is intended for information purposes only. It is not intended to reflect any recommendation or financial advice and investment decisions should not be based on it. This information does not constitute an offer, a solicitation of an offer, or an inducement to subscribe for, purchase or sell any financial instrument or to enter into a legally binding contract. To the extent that this information contains any general advice, it has been prepared without taking into account your objectives, financial situation or needs and before acting on it you should consider the appropriateness of the advice. Certain types of transactions, including those involving futures, options and high yield securities give rise to substantial risk and are not suitable for all investors. We recommend that you seek your own independent legal or financial advice before proceeding with any investment decision. This information may contain material provided by third parties. While such material is published with the necessary permission none of Westpac or its related entities accepts any responsibility for the accuracy or completeness of any such material. Although we have made every effort to ensure this information is free from error, none of Westpac or its related entities warrants the accuracy, adequacy or completeness of this information, or otherwise endorses it in any way. Except where contrary to law, Westpac Group intend by this notice to exclude liability for this information. This information is subject to change without notice and none of Westpac or its related entities is under any obligation to update this information or correct any inaccuracy which may become apparent at a later date. This information may contain or incorporate by reference forward-looking statements. The words “believe”, “anticipate”, “expect”, “intend”, “plan”, “predict”, “continue”, “assume”, “positioned”, “may”, “will”, “should”, “shall”, “risk” and other similar expressions that are predictions of or indicate future events and future trends identify forward-looking statements. These forward-looking statements include all matters that are not historical facts. Past performance is not a reliable indicator of future performance, nor are forecasts of future performance. Whilst every effort has been taken to ensure that the assumptions on which any forecasts are based are reasonable, the forecasts may be affected by incorrect assumptions or by known or unknown risks and uncertainties. The ultimate outcomes may differ substantially from any forecasts.

Conflicts of Interest: In the normal course of offering banking products and services to its clients, the Westpac Group may act in several capacities (including issuer, market maker, underwriter, distributor, swap counterparty and calculation agent) simultaneously with respect to a financial instrument, giving rise to potential conflicts of interest which may impact the performance of a financial instrument. The Westpac Group may at any time transact or hold a position (including hedging and trading positions) for its own account or the account of a client in any financial instrument which may impact the performance of that financial instrument.

Author(s) disclaimer and declaration: The author(s) confirms that no part of his/her compensation was, is, or will be, directly or indirectly, related to any views or (if applicable) recommendations expressed in this material. The author(s) also confirms that this material accurately reflects his/her personal views about the financial products, companies or issuers (if applicable) and is based on sources reasonably believed to be reliable and accurate.

Further important information regarding sustainability-related content: This material may contain statements relating to environmental, social and governance (ESG) topics. These are subject to known and unknown risks, and there are significant uncertainties, limitations, risks and assumptions in the metrics, modelling, data, scenarios, reporting and analysis on which the statements rely. In particular, these areas are rapidly evolving and maturing, and there are variations in approaches and common standards and practice, as well as uncertainty around future related policy and legislation. Some material may include information derived from publicly available sources that have not been independently verified. No representation or warranty is made as to the accuracy, completeness or reliability of the information. There is a risk that the analysis, estimates, judgements, assumptions, views, models, scenarios or projections used may turn out to be incorrect. These risks may cause actual outcomes to differ materially from those expressed or implied. The ESG-related statements in this material do not constitute advice, nor are they guarantees or predictions of future performance, and Westpac gives no representation, warranty or assurance (including as to the quality, accuracy or completeness of the statements). You should seek your own independent advice.

Additional country disclosures:

Australia: Westpac holds an Australian Financial Services Licence (No. 233714). You can access Westpac’s Financial Services Guide here or request a copy from your Westpac point of contact. To the extent that this information contains any general advice, it has been prepared without taking into account your objectives, financial situation or needs and before acting on it you should consider the appropriateness of the advice.

New Zealand: In New Zealand, Westpac Institutional Bank refers to the brand under which products and services are provided by either Westpac (NZ division) or Westpac New Zealand Limited (company number 1763882), the New Zealand incorporated subsidiary of Westpac ("WNZL"). Any product or service made available by WNZL does not represent an offer from Westpac or any of its subsidiaries (other than WNZL). Neither Westpac nor its other subsidiaries guarantee or otherwise support the performance of WNZL in respect of any such product. WNZL is not an authorised deposit-taking institution for the purposes of Australian prudential standards. The current disclosure statements for the New Zealand branch of Westpac and WNZL can be obtained at the internet address www.westpac.co.nz .

Singapore: This material has been prepared and issued for distribution in Singapore to institutional investors, accredited investors and expert investors (as defined in the applicable Singapore laws and regulations) only. Recipients of this material in Singapore should contact Westpac Singapore Branch in respect of any matters arising from, or in connection with, this material. Westpac Singapore Branch holds a wholesale banking licence and is subject to supervision by the Monetary Authority of Singapore.

U.S.: Westpac operates in the United States of America as a federally licensed branch, regulated by the Office of the Comptroller of the Currency. Westpac is also registered with the US Commodity Futures Trading Commission (“CFTC”) as a Swap Dealer, but is neither registered as, or affiliated with, a Futures Commission Merchant registered with the US CFTC. The services and products referenced above are not insured by the Federal Deposit Insurance Corporation (“FDIC”). Westpac Capital Markets, LLC (‘WCM’), a wholly-owned subsidiary of Westpac, is a broker-dealer registered under the U.S. Securities Exchange Act of 1934 (‘the Exchange Act’) and member of the Financial Industry Regulatory Authority (‘FINRA’). This communication is provided for distribution to U.S. institutional investors in reliance on the exemption from registration provided by Rule 15a-6 under the Exchange Act and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors in the United States. WCM is the U.S. distributor of this communication and accepts responsibility for the contents of this communication. Transactions by U.S. customers of any securities referenced herein should be effected through WCM. All disclaimers set out with respect to Westpac apply equally to WCM. If you would like to speak to someone regarding any security mentioned herein, please contact WCM on +1 212 389 1269. Investing in any non-U.S. securities or related financial instruments mentioned in this communication may present certain risks. The securities of non-U.S. issuers may not be registered with, or be subject to the regulations of, the SEC in the United States. Information on such non-U.S. securities or related financial instruments may be limited. Non-U.S. companies may not be subject to audit and reporting standards and regulatory requirements comparable to those in effect in the United States. The value of any investment or income from any securities or related derivative instruments denominated in a currency other than U.S. dollars is subject to exchange rate fluctuations that may have a positive or adverse effect on the value of or income from such securities or related derivative instruments.

The author of this communication is employed by Westpac and is not registered or qualified as a research analyst, representative, or associated person of WCM or any other U.S. broker-dealer under the rules of FINRA, any other U.S. self-regulatory organisation, or the laws, rules or regulations of any State. Unless otherwise specifically stated, the views expressed herein are solely those of the author and may differ from the information, views or analysis expressed by Westpac and/or its affiliates.

UK and EU: The London branch of Westpac is authorised in the United Kingdom by the Prudential Regulation Authority (PRA) and is subject to regulation by the Financial Conduct Authority (FCA) and limited regulation by the PRA (Financial Services Register number: 124586). The London branch of Westpac is registered at Companies House as a branch established in the United Kingdom (Branch No. BR000106). Details about the extent of the regulation of Westpac’s London branch by the PRA are available from us on request.

Westpac Europe GmbH (“WEG”) is authorised in Germany by the Federal Financial Supervision Authority (‘BaFin’) and subject to its regulation. WEG’s supervisory authorities are BaFin and the German Federal Bank (‘Deutsche Bundesbank’). WEG is registered with the commercial register (‘Handelsregister’) of the local court of Frankfurt am Main under registration number HRB 118483. In accordance with APRA’s Prudential Standard 222 ‘Association with Related Entities’, Westpac does not stand behind WEG other than as provided for in certain legal agreements (a risk transfer, sub-participation and collateral agreement) between Westpac and WEG and obligations of WEG do not represent liabilities of Westpac.

This communication is not intended for distribution to, or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. This communication is not being made to or distributed to, and must not be passed on to, the general public in the United Kingdom. Rather, this communication is being made only to and is directed at (a) those persons falling within the definition of Investment Professionals (set out in Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”)); (b) those persons falling within the definition of high net worth companies, unincorporated associations etc. (set out in Article 49(2)of the Order; (c) other persons to whom it may lawfully be communicated in accordance with the Order or (d) any persons to whom it may otherwise lawfully be made (all such persons together being referred to as “relevant persons”). Any person who is not a relevant person should not act or rely on this communication or any of its contents. In the same way, the information contained in this communication is intended for “eligible counterparties” and “professional clients” as defined by the rules of the Financial Conduct Authority and is not intended for “retail clients”. Westpac expressly prohibits you from passing on the information in this communication to any third party.

This communication contains general commentary, research, and market colour. The communication does not constitute investment advice. The material may contain an ‘investment recommendation’ and/or ‘information recommending or suggesting an investment’, both as defined in Regulation (EU) No 596/2014 (including as applicable in the United Kingdom) (“MAR”). In accordance with the relevant provisions of MAR, reasonable care has been taken to ensure that the material has been objectively presented and that interests or conflicts of interest of the sender concerning the financial instruments to which that information relates have been disclosed.

Investment recommendations must be read alongside the specific disclosure which accompanies them and the general disclosure which can be found here. Such disclosure fulfils certain additional information requirements of MAR and associated delegated legislation and by accepting this communication you acknowledge that you are aware of the existence of such additional disclosure and its contents.

To the extent this communication comprises an investment recommendation it is classified as non-independent research. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and therefore constitutes a marketing communication. Further, this communication is not subject to any prohibition on dealing ahead of the dissemination of investment research.